The Margin Paradox: Axis Bank's Profit Surge Masks a Cyclical Low in NIM

Axis Bank's Q1 FY27 earnings present a fascinating paradox of modern banking: a robust 23% surge in net profit achieved even as its Net Interest Margin (NIM) compressed to a cyclical low. This performance highlights a strategic pivot toward non-interest income and volume growth to offset the headwinds of rising funding costs.

The Paradox of Profitability: Deconstructing Axis Bank's Q1 FY27 Performance

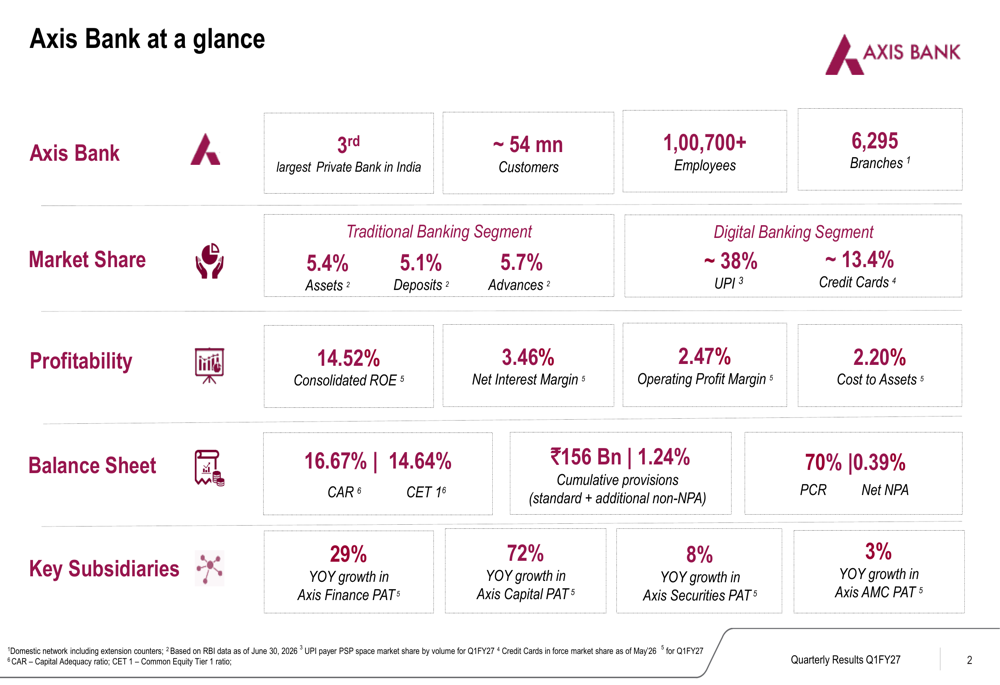

The financial results of Axis Bank for the first quarter of fiscal year 2027 have presented a complex narrative for banking analysts and investors alike. According to a report by Investing.com, the prominent Indian private sector lender delivered a stellar 23% year-on-year surge in net profit. However, beneath this headline-grabbing growth lies a critical vulnerability: the bank's Net Interest Margin (NIM) has compressed to its lowest point in the current credit cycle.

This divergence highlights a classic banking paradox. While the core profitability rate of the bank's lending activities—the spread between interest earned and interest paid—is being squeezed, the institution has successfully offset this headwind through sheer volume growth and diversification of non-interest income streams. This performance offers valuable lessons for global financial institutions navigating prolonged high-interest-rate environments.

NIM Compression: The Cost of Deposits and Tight Liquidity

The primary catalyst behind Axis Bank's cyclical low in NIM is the escalating cost of funds. As the Reserve Bank of India (RBI) maintains a tight monetary stance to curb inflation, system-wide liquidity has remained constrained. This has triggered intense competition among banks to secure retail deposits, forcing institutions to offer higher interest rates to attract and retain depositors.

Furthermore, there has been a noticeable structural shift in deposit composition. Customers are increasingly migrating their funds from low-cost Current Account and Savings Account (CASA) deposits into high-yield term deposits. This shift has significantly increased the bank's interest expenses, leading to the inevitable compression of net interest margins despite robust credit demand.

Volume and Fees: The Engines of Growth

How did Axis Bank manage a 23% profit surge in the face of such margin pressure? The answer lies in a dual strategy of aggressive loan book expansion and robust non-interest income growth. By expanding its credit portfolio across retail, SME, and corporate segments, the bank increased the absolute volume of its interest-earning assets, effectively compensating for the lower margin per unit.

Additionally, fee-based income—driven by wealth management services, credit card fees, and investment banking activities—provided a crucial buffer. Combined with stringent operational cost management and stable asset quality that kept provisioning requirements in check, Axis Bank demonstrated remarkable resilience in its bottom-line performance.

Strategic Outlook for the Indian Banking Sector

Axis Bank's Q1 FY27 results serve as a bellwether for the broader Indian banking sector. As long as liquidity remains tight and deposit rates stay elevated, banks will need to look beyond traditional net interest income. Success in the upcoming quarters will likely be determined by an institution's ability to cross-sell products, leverage digital channels to lower acquisition costs, and maintain pristine asset quality.

When it comes to understanding the big market picture and forming investment strategies, FireMarkets' Market Insight provides broad perspectives from macroeconomic analysis to individual asset trends. Monitoring how major lenders like Axis Bank navigate this margin-volume trade-off will be essential for investors looking to capitalize on India's dynamic financial sector.

FireMarkets Intelligent Outlook

Real-time technical analysis and AI sentiment for 532215, AXISBANK.NS.

View AI Analysis Summary

Firemarkets.net AI Analysis Result:

* Not financial advice. Data for informational purposes only.

Want deeper analysis on this asset?

Check out expert reports and on-chain data provided by FireMarkets specialists.

All content provided by FireMarkets (including news, analysis, and data) is for reference purposes only to assist in investment decisions and does not constitute a recommendation to buy or sell any specific asset.

Financial markets are highly volatile, and past performance is not indicative of future results. Please rely on your own judgment and consult with professionals before making any investment decisions. FireMarkets assumes no legal liability for investment outcomes.